Workers’ comp explained

Before we start explaining how to find how much workers’ compensation you pay on a per employee basis, we first need to briefly go over what it is all about. It is a system that provides protection for employers from lawsuits by workers injured while working and allows them to provide benefits to these employees, no matter whose fault it is. For instance, even if your bookkeeper uses his rolling chair as a ladder and falls and breaks an arm, he will still be paid the workers’ compensation.

If your cashier, let’s say, fell on a slippery floor and broke her leg, the employer would need to pay the ambulance ride to the hospital and all of the medical expenses she incurs while at the hospital. If the employer has workers’ comp insurance, these costs are covered by the workers’ compensation. So any costs associated with tests, medications, and even surgeries are covered.

Ongoing care, such as doctor’s appointments and follow-up surgeries, is also covered. Moreover, if the cashier is unable to return to work after a certain period of time, which typically ranges from three to seven days, the workers’ comp would also pay for wage replacement.

When it comes to insurance, this type of coverage is often one of the largest expenses a business has. Even though the state laws set the requirements and this insurance compulsory or not compulsory, it would typically cost the business much less to pay the insurance than to cover all the costs in relation to the employee’s injury.

It is one of the greatest benefits that an employer can provide to its employees. Moreover, the employees legally surrender their rights to sue the company that hired them for any sort of negligence in exchange for these benefits. Finally, if you are legally required to have this insurance by your state and fail to get one, you can pay a significant fee or be imprisoned, or both. Thus, if you are still wondering if you should get workers’ comp, then you can be confident that the benefits outweigh the costs. Nonetheless, it never hurts to know how much each employee will cost for more effective management of your business costs.

How is it estimated?

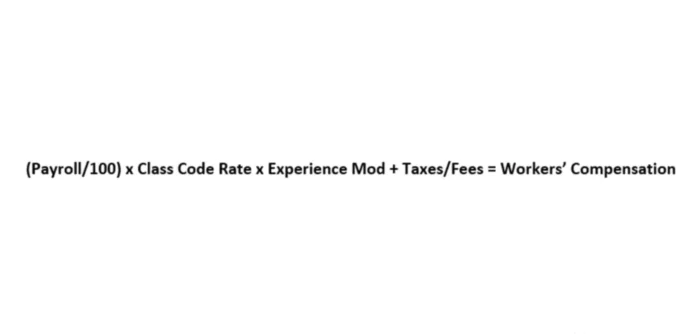

It is helpful to understand how the premium is actually derived. Insurance carriers assign a unique rate to each business (client). There are three main factors that are considered when they make their rate estimates. These are class codes, payroll, and experience mod. The calculation is relatively simple.

- PayrollHow much an employer pays for the workers’ compensation benefits depends on how much its employees earn You would take the total reportable payroll divided by 100. When calculating the total, you would add up the gross earnings of each and every employee, no matter if they work part or full-time or even if it is just a worker who is not going to stay on a long-term basisWhen it comes to independent contractors, the rules on whether or not you should pay for them depend on where your company is located. If you are not sure who exactly should be included in the total, look for information provided by your state.For employees who earn hourly wages, you can use their estimated earnings for the year ahead. To further simplify the calculations, it is possible to round the numbers to the nearest one thousand. If your driver makes $65,800, you can enter $66,000 in the calculations. Do not worry if your calculations are not very exact because you can make some adjustments later when you know how much you actually paid the workers.

- Class codesYour next step is to find respective classification codes. If you had some wiggle room with your calculations in the first step, here you need to make sure you get everything right. What are these codes? These are codes that the companies that provide insurance for your workers use to identify specific categories of work. In other words, to make it simpler for themselves, instead of using job titles to describe a job and associated tasks and responsibilities, the insurance providers use codes. For instance, a cashier would correspond to a number 1234.They need to categorize various types of positions using codes to know what they should be planning to cover and how much they should charge for it. A builder, for instance, will have a more expensive rate compared to an office worker who just sits in front of a computer the whole day and does not perform any type of dangerous work.

- Experience modThe providers of insurance coverage also assign a number that corresponds to the injury history of the organization. Simply put, this is a score you get as a business for the effectiveness of your injury prevention and safety measures. A business that promotes safety and has a great experience modifier or mod below one will pay less and potentially receive credits, thus further reducing the premium, than an entity that has a higher mod and has less than favorable risk management practices.How is this number assigned? Well, insurance companies compare all the companies in the industry and see how a particular entity stacks up against other companies. For instance, construction companies are compared with other construction companies, and automobile companies are compared to other automobile companies. After all, the insurance company has to plan how much it might need to pay your company based on average workplace injuries in a particular industry, which is represented by a mod 1.00. It ultimately determines how much you pay.

- Workers’ Comp RateAlthough every class has a kind of a standard rate, which is determined by a special organization in every state separately, these are typically used only as a guide and the actual rates are likely to be different from what is recommended. How much they deviate will depend on the insurance provider and, of course, other indicators, such as your experience mod. It is presented as a cost per $100 each and every employee covered by the insurance earn. In other words, if a business is offered a rate of $0.58, it will pay $580 annually for every $100,000 it pays in payroll.

Per Employee Calculation

The previous steps help you to see how the total annual amount is determined for a particular company. Now, we are going to explain how to find its cost for each employee. You would need to take the employee’s pay and divide it by 100 because the rate is presented for every $100 earned. So, if John has an annual gross pay of $48,800 and you divide it by 100, you will get $488.

Your next step is to assign a class code for John and the corresponding insurance rate either from what your state gives or the specific insurance provider. The value you have arrived at earlier is then multiplied by this rate. Let’s say that for the type of work John performs in your company it is $1.36. Thus, we can say that your cost per employee is $488 x $1.36 or $663.68 per year.

Of course, you do not need to calculate it for each employee separately. Your business is likely to have employees that fall under the same class code. Thus, instead of doing it for each and every individual on your payroll, you would add the gross pay of all employees that fall under one class code and calculate the insurance costs per employee for each category separately.

It might seem that whatever you get is kind of a set-in-stone number. However, there are several ways you can reduce these costs and not by simply searching for a different provider. What you want to focus on is the indicator you do have control over or the experience modifier. When talking to the insurance agency, make sure that your company is focused on safety and have a good backup for your words. Remember, no one is prevented from unfortunate life events, but we can make them less stressful for us.