One of the steps in the accounting cycle is balancing off the accounts. You can do this after all the financial data has been posted to the ledger accounts. What does it mean? Balancing off means matching figures of debits and credits of the account.

What is a Balance

It represents the amount that is the same in both columns of an account. In case amounts do not match, you should put the difference in the column with a lesser amount. If the debit consists of the larger figure, the balance is called a debit balance. Similarly, if the credit has a higher amount, it means the account has a credit balance.

Balancing off Accounts Process

This procedure can be straightforward if we are dealing with one type of entry. We add up all the entries to make sure the totals of the ledger account balance.

In a case of more than one entry, you should follow some procedures as described below:

- Calculate the total figures in both columns of the ledger account;

- Figure out any discrepancies between the two columns.

- Enter it in the column of the ledger with the smaller amount, so that both sides are made equal. This is to be the balance c/f (carried forward);

- That amount of the balance c/f should be written in the column with the greater total. The term for it is the balance b/f (brought forward);

Example of Balancing off Accounts

To better understand how this process works, you would follow the necessary steps, as shown here:

- Find the larger total by totaling both sides of the account, which, in our case, is 5,370. In this example, the figure is larger on the debit side;

- Enter the higher amount in the total line on both sides, debit 5,370, credit 5,370;

- Calculate the discrepancy between the large side and the small side (5,370-400=4,970) and set the figure in the small side naming it to balance carried forward (c/f). In this case, it’s the credit;

- The balance b/f is inserted to the debit column just below the totals line. This is going to be the closing balance for that particular period.

Balancing off Accounts with a Credit Balance

As we mentioned in the beginning, for the ledger account to have a credit balance, the amount of the credits must be greater than the debit figure.

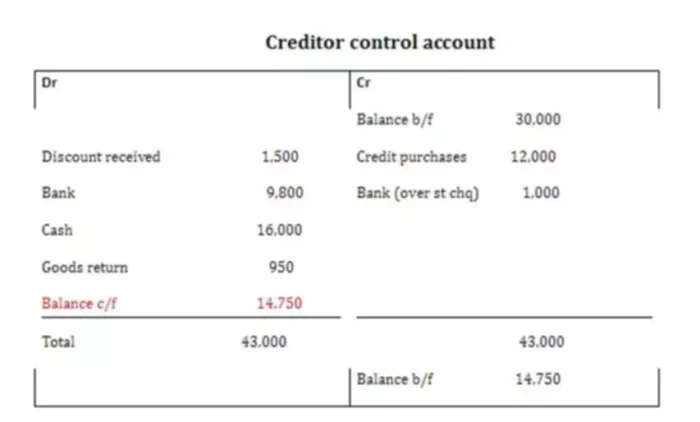

Here is the illustration of the creditor control account:

The process of balancing off in this table is similar to the previous example. The first step is the calculation of the totals of the debit and credit sides. Next, the higher total is inserted as the total of both columns, leaving a line above totals to add the extra entry on the lower side. Any difference of the totals is then written on that line as the balance c/f. The balance b/f is going below the totals of the account.

Permanent and Temporary Accounts

Every account is either permanent or temporary, for the most part.

Let’s first take a look at the temporary ones.

According to fundamental principles of accountancy, the term for temporary accounts means that they zero out as of the end of the closing process so that we can start the next period.

There are certain accounts, such as revenue accounts, expense accounts, and the withdrawals that are temporary.

Assume we have $25,000 in revenue this year, then next year, we want to start over at zero and start accumulating our revenue for the next year. Every single year we want to know how much revenue we have for that year, how much revenue we have to the next year, so that’s why it’s a temporary account. That doesn’t mean we get rid of the account, and it just means the balance is temporary.

At the end of the year, we need to eliminate that account balance to start the year at zero, and then we track the new balance for that year.

As for permanent accounts, these are accounts that generate the balance sheet accounts that do not go away in the closing process, unlike the temporary accounts.

The permanent accounts are our asset accounts, our liability accounts, and then our capital account. The balances of these accounts we don’t zero out at the end of the year.

If you have a $100,000 in your account on December 31, then on January 1, when you open up, you’re not going to zero that account out, you’re going to start with a $100,000 the next year. That’s how all assets are going to work.

You’re going to carry the balance from December 31 over into January 1, whereas for the temporary accounts, the December 31 balance will then be zeroed out at the end of the day. On January 1, you should start with brand new balances to track next year’s transactions.