Accounting is an integral part of any enterprise. Controlling financial data lets you make rational decisions regardless of your approach to firm management. Therefore, firms, especially those who plan to expand their business, should study the main retail accounting techniques.

Although retail accounting is not a separate type of financial activity, it does have some characteristics, e.g., increased attention to inventory, which we will discuss in this blog post.

In a changing financial environment, you must recognize the different accounting methods you can adopt. This article will assist you in selecting the appropriate retail accounting method.

Understanding retail accounting

Retail accounting includes a non-standard technique that allows organizations to monitor inventory without manually counting all products in storage or trading floors. This kind of financial activity transforms your stocks into their evaluated commercial value.

The calculation shows how many commodities the firm has at its disposal at the end of a certain period.

This retail method assists in defining the percentage markup of items shipped by identifying how much inventory you have based on the volume of commodities sold.

Knowing this data is critical for several reasons, including how many products are available, e.g., before generating financial documents or assessing the firm’s current position.

Retail method formula

The retail method is defined as calculating the ratio of cost to commercial value to evaluate the inventory cost. To understand the price of inventory as of the end of the period, you need to adhere to the following process:

- Record all purchases and commodities on hand at cost and commercial price.

- Compute cost-to-retail ratio with formula: Cost price*100 / Commercial price.

- Evaluate inventory at the retail price after deducting the value of sold commodities from the retail cost of commodities in reserves.

- Convert the commercial value of stock to the cost price using cost-to-retail ratios.

Take the following step-by-step example:

- Suppose you purchased commodities for $85 and resold them for $125; the cost-to-retail ratio is 68%.

- The initial cost of stock is $2,000, and you purchased $3,000 of inventory. Simultaneously, your sales amounted to $6,000.

- Compute the sum of inventory: initial stock + purchases = products that are accessible for sale as follows:

$2,000 + $3,000 = $5,000 - Then estimate the final inventory: accessible products – sales (shipment volumes* cost-to-retail parameter) = Final inventory

$,5000 – ($6,000*68%) = $920

Retail accounting for inventory management

Understanding how to monitor inventory is crucial, particularly when dealing with multiple production units with various costs. In such cases, selecting a framework to determine the cost of goods sold becomes essential for comparing it with ending inventories and establishing earnings. To achieve this, it is necessary to establish cost-flow assumptions. It’s important to note that the system doesn’t control the physical movement of sold products but rather attributes a value to inventory, allowing for a more accurate calculation of profits.

It is possible to achieve this in different ways. Below, we will analyze four popular cost accounting techniques to track your inventory.

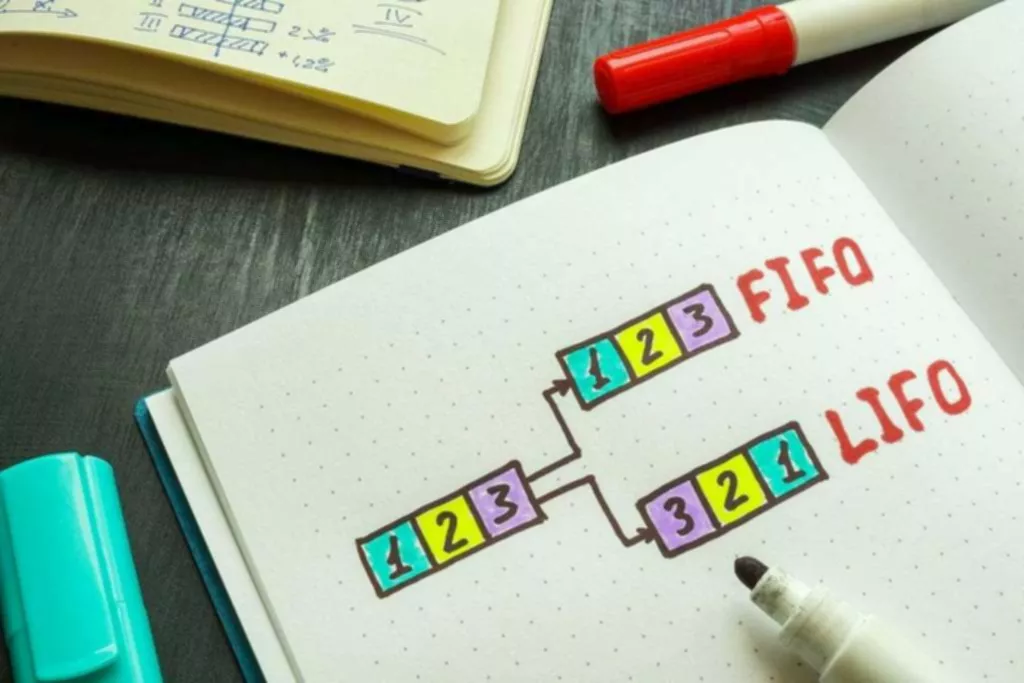

LIFO

The LIFO retail method states that the last item purchased in the business’s inventory will be sold first.

Example: Suppose you bought 200 phone cases at $6, 300 phone cases at $7, and 500 phone cases at $8. It means the first 500 items sold will be valued at $8 per unit, the next 300 – $7, and the last 200 – $6 since new ones are considered first-to-go goods.

LIFO accounting is utilized when it is difficult to distinguish one unit of inventory from another, and inventories will not be rotated to guarantee that old inventories fly out first. Firms that engage in bulk supplies of sand or gravel choose the LIFO accounting algorithm.

FIFO

FIFO accounting is the opposite of LIFO, meaning the first thing that enters your reserves will be the first thing you sell. The FIFO formula states that expenditures for purchasing inventory are recognized first.

Example: Suppose you bought 200 phone cases at $6, 300 units at $7, and 500 phone cases at $8. FIFO will assign a price of $6 for the first item sold. After selling 200 products, the new price will be $7; the last 500 products will have a price of $8 since the methodology provides for the oldest product to be sold at the beginning.

This retail method is most suitable when we speak about products that quickly spoil. It is used by firms that sell food products.

Weighted average

The weighted average falls in between LIFO and FIFO stock evaluation methods. This weighted average technique averages the value of all commodities without regard to order.

Example: Suppose you got 200 phone cases at $6, 300 units at $70, and 500 phone cases at $80. These are the only things you had on hand. The first category accounted for 20% of total inventory, the second – 30%, and the third – 50%.

The weighted average cost is: $6*20% + $7*30% + $8*50% = $7.30

Specific identification

Specific identification cost technique is the most basic option for controlling inventories. You need to monitor each component individually and not think about what you will sell first. Specific identification is best used in commercial sites with limited product quantities, higher prices, and low-volume operations. It is simpler for a car dealership or appliance store to keep track of each component in inventory than in a supermarket. If your firm can utilize specific identification, the IRS demands you do so.

Advantages and disadvantages of retail accounting

The retail method stands as a fast and simple approach to compute inventory. The primary advantage of this technique is that it does not involve the organization of actual inventory. Let’s explore other benefits of this formula:

- Comfort: When using this accounting method, the value of your physical inventory is not as critical as understanding the commercial value of your commodities.

- Cutting costs: While manual inventory tracking remains essential, you won’t have to do it as often. This decreases costs because you are no longer doing work manually during non-working hours.

- Ability to prepare financial papers: The retail accounting method allows you to prepare reports on the inventory cost for budgeting and generate reports.

Like any other technique, retail accounting has some downsides:

- Low accuracy when prices change: If the value of your commodities constantly evolves, the retail method may not be accurate. Constant price changes violate the primary principle of accounting that all production units have the same cost and rate of price change.

- Estimates rather than accurate figures: Because the approach creates unreal pricing conditions, it only estimates stock values instead of providing exact numbers.

The approach is suitable if you value convenience and ease of accounting. But remember there are exceptions e.g., products with discounts, sales, or markups because such approach accounting in its basic version does not consider them.

Retail vs. cost inventory accounting

Some organizations prefer cost accounting, which has some different features than retail accounting. Retail accounting is based on the evaluated price of purchase. Cost accounting is more sophisticated because it examines various factors, including transportation, production spending, overhead expenditures, etc.

Financial experts say cost accounting provides greater precision but involves complex computation. The primary benefit of retail accounting is that you instantly define the value of your inventories since your customers pay this price. Researching factors related to cost accounting can be difficult because many conditions are out of your control as an entrepreneur.

Decent retail accounting practice elements

Retail accounting can be a severe problem, especially for firms with diverse inventories and significant volume of operations. We have collected several retail recommendations that will make your commercial structure as efficient as possible:

- Open a business bank account: A separate bank account is a prerequisite to the successful operation of a firm.

- Use cutting-edge software: A reliable accounting program will make many business aspects more manageable.

- Manage inventories: Cash inflows shape product outflows. Maintaining a steady supply of goods is essential, but predicting how quickly your goods will sell can be challenging.

- Select your accounting method carefully: Enterprises must obtain a resolution from the IRS to change their accounting methods, including the approach of inventory valuation. Since there is no guarantee you will get such approval, you must carefully select your methods.

As a retailer, you probably use many accounting techniques described in this blog. In particular, retail accounting is more straightforward and convenient and provides significant savings in working hours in the long term, but it also has some downsides.

As the enterprise develops, your financial processes will grow along with it. Are you ready to outsource your retail or cost accounting? Schedule an online consultation with BooksTime experts today to learn how we can help your business to grow. You can focus on your products, employees, and customers. Don’t wait until your accounting problems become too difficult to manage – tackle them now.