Accurate record-keeping plays a vital role in managing your finances and making informed business decisions. However, setting up and maintaining your accounting books requires a basic understanding of accounting terminology. What is a normal balance of accounts? Which account has a normal credit balance and which one has a normal debit balance? Read this article to learn more, or reach out to a qualified financial adviser at BooksTime for a FREE consultation.

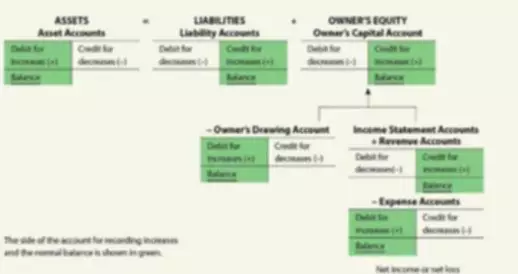

Normal Balance and the Accounting Equation

Accountants generally utilize the double-entry method of bookkeeping which means that every business transaction should have at least two corresponding journal entries: a debit and a credit.

The Accounting Equation is considered to be the foundation of double-entry bookkeeping. It’s a basic principle whereby Assets = Liabilities + Owner’s Equity (A=L+OE). The Accounting Equation determines whether an account increases with a debit or a credit entry. The normal balance is part of the double-entry bookkeeping method and refers to the expected debit or credit balance in a specified account. For example, accounts on the left-hand side of the accounting equation will increase with a debit entry and will have a debit (DR) normal balance. Accounts on the right-hand side of the accounting equation will have a normal credit (CR) balance.

Below is a list of the standard accounts and their expected normal balance:

- Asset: Debit

- Expense: Debit

- Dividends: Debit

- Liability: Credit

- Owner’s Equity: Credit

- Revenue: Credit

- Retained Earnings: Credit

Normal Balance Examples

We can explain normal balance using an example. Let’s say you own a café and you purchase $450 of coffee beans from your local supplier. You’re sitting down in the evening to update your books, and you’re presently recording all of your accounting transactions by hand. Using the double-entry method of bookkeeping, you will record the transaction twice: one entry under the Cash account to decrease it, and one entry under the Supplies account to show an increase in supply. Both accounts belong to Assets, so they have a normal debit balance and will increase with a debit entry and decrease with a credit entry.

Let’s look at another example. Let’s assume that you deposit $10,000 into your business account. When recording this transaction, you’ll make one entry under “Bank” (because money is being received) and one entry under “Capital” (because cash put into the business by the owner is allocated to the Capital account). The Bank account is an Asset account which means it has a normal debit balance. The capital account is an Owner’s Equity account which means it has a normal credit balance.

Contra Accounts

Contra accounts are individual accounts that are established to decrease the balance in another account indirectly by netting the two accounts together in the General Ledger. They are “backwards” accounts which means that their normal balances are opposite of the normal balances of their corresponding account(s).

Below are some examples of Primary Accounts with a normal debit balance and their corresponding Contra Accounts which, in turn, have a normal credit balance:

- Accounts Receivable – Allowance for Doubtful Accounts

- Fixed Assets – Accumulated Depreciation

- Intangible Assets – Accumulated Amortization

- Sales Revenue – Sales Returns and Allowance / Sales Discounts

- Loans Receivable – Allowance for Doubtful Loans

An example of a contra asset account is ‘Accumulated Depreciation’. A company invests in a truck. The truck cost the company $35,000 which depreciated by $6,000. Therefore, the carrying amount (or book value) of the truck is $29,000.

Using the Normal Balance

Double-entry bookkeeping enables businesses to maintain accurate and reliable financial records. This method of recording financial transactions would not exist without the normal balance.

It’s important to note that an account that has a normal credit balance can have a debit balance or not. This may occur due to an error when recording entries. Knowing what the normal balance for a particular account should be is important in order to easily identify data entry mistakes.

There are other reasons for an account with a normal credit balance to show a debit balance or vice versa. This result may be attributed to an entry reversing a transaction that was in a prior year and already zeroed out of the account. Or, a bookkeeper may have made an offsetting entry prior to the entry it was intended to offset. If you notice an account doesn’t display the normal balance as expected, it’s a red flag. If the reason why is not immediately obvious, it’s a good idea to consult with your bookkeeper or accountant ASAP.

Normal Balances of Accounts Chart

We now know that each account has either a credit normal balance or a debit normal balance. When looking at the expanded accounting equation: Assets + Expenses + Dividends + Losses = Liabilities + Capital + Revenue + Gains, it is much easier to determine which account has a credit or a debit normal balance. In the table below, you can check the normal balances of different types of accounts and see how debit and credit entries affect them.

Need assistance setting-up and maintaining your books?

Running a business is hard enough. And while bookkeeping is a necessary part of running a successful business, manual bookkeeping can be time-consuming and prone to error, potentially costing you more than the savings of doing it yourself are worth. At Bookstime, we are happy to help. Fill out this form(hyperlink) to schedule a free consultation with one of our Bookkeepers now.